Memo Published June 1, 2020 · 12 minute read

Mapping the Progress and Potential of Carbon Capture, Use, and Storage

Matt Bright

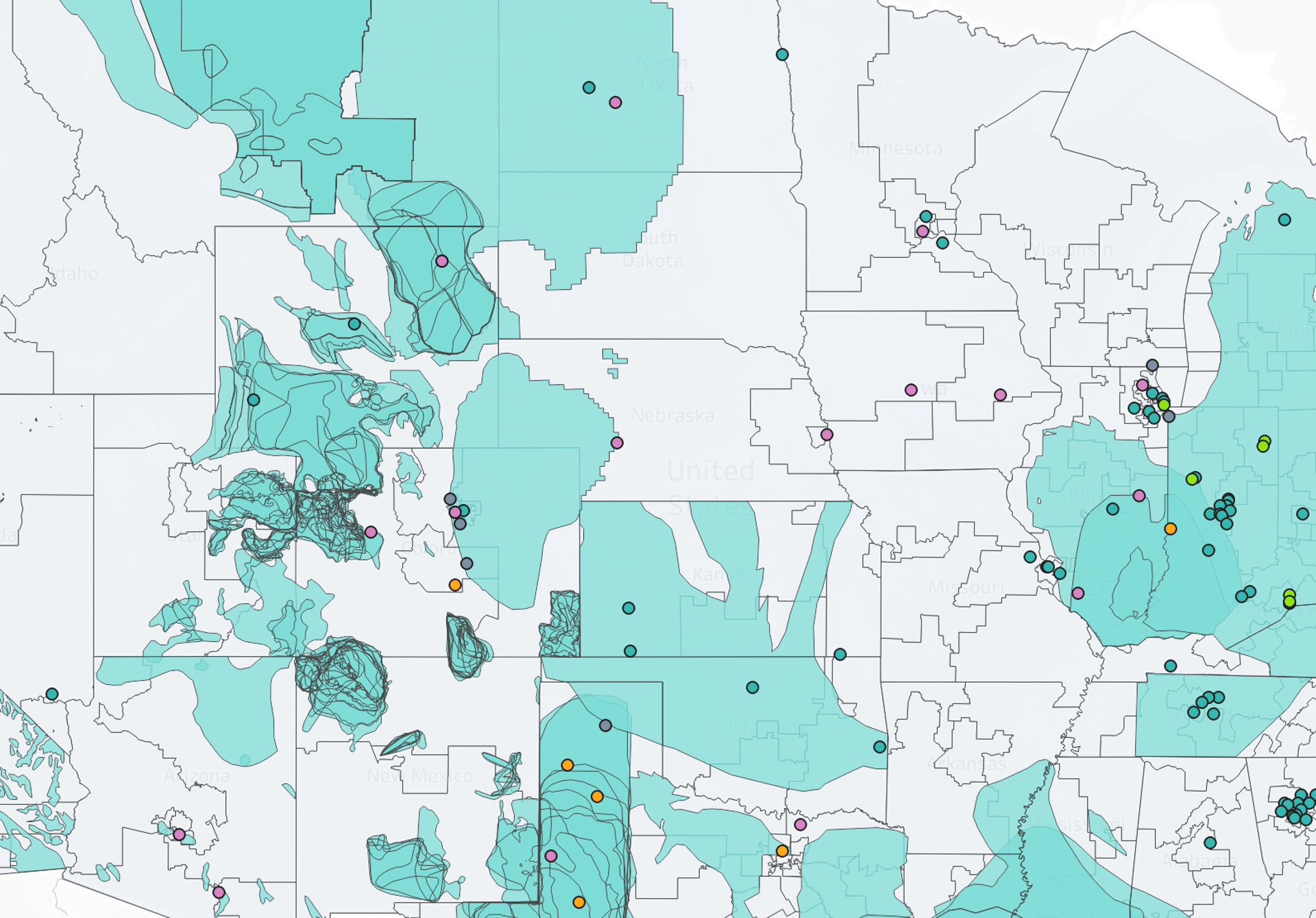

It’s a fact: our latest projects map shows that the carbon capture, use, and storage (CCUS) universe is expanding! CCUS is critical for achieving climate goals and also provides huge opportunities for economic growth across the country. That’s why the buzz of new activity in this space over the past two years is so exciting. While additional policy supports will be needed to accelerate CCUS deployment, momentum is clearly building. Below are a few encouraging highlights of the progress made since Third Way released the 2018 version of our Carbon Capture Projects Map:

- The number of carbon capture projects being planned, constructed, or operated worldwide has jumped 32%, from 300 to 396.

- Of the 96 new additions, 62 are in the United States.

- CCUS projects are found in 37 states and the District of Columbia.

- New projects in the power generation and industrial sectors demonstrate that CCUS is a serious weapon in the climate change fight.

- Many projects are using novel technologies, showing continued innovation in CCUS.

You can explore the updated 2020 interactive map below. This memo also includes a recap of some of the biggest trends in the CCUS industry, and a few basic policy principles to help carbon capture reach its full economic and climate potential and put many more projects on the map.

Our 2020 map includes several new features that will make it easier for policymakers and advocates to find useful information on CCUS projects. First, the map contains three new layers that show: 1) where carbon dioxide can be permanently sequestered in saline sandstone basins thousands of feet below the surface; 2) where carbon dioxide can be used and stored in enhanced oil recovery fields; and 3) the Congressional districts where U.S. carbon capture projects are located. Second, we’ve made it easier to see how much carbon is being captured, used, or stored by different projects. Finally, we’ve added short descriptions of each project to our database, along with a link to project developer websites. For more details on how to use the map and Third Way’s methodology, click here.

What Lessons Can We Take Away from the New CCUS Map?

In the following paragraphs, we delve into the current state of global projects in the six major applications for carbon capture technologies, focusing on recent additions and noteworthy developments that have arisen during the past two years.

Power Generation

The United States power sector has seen an uptick in recent CCUS activity. Our map identifies nine new projects at power generating facilities, all in the U.S., bringing the global total up to 78. Seven of these new projects are known as front-end, engineering design (FEED) studies on coal or natural gas-fired power plants funded by the U.S. Department of Energy.1 FEED studies are a critical step in the RD&D pipeline and help developers learn how to scale a project up to commercially deployable capture rates. One of the FEED studies, Project Tundra in North Dakota, would retrofit a coal-fired power plant to capture three million metric tons per year (tpy) of CO2 and permanently sequester it a mile underneath the facility. If successful, this would be one of the world’s largest carbon capture facilities. If all seven of the new FEED studies led to commercial-scale deployment, they would eliminate 17.2 million tons of CO2 emissions each year, or 1% of annual U.S. emissions from coal and natural gas-fired power plants.2

We’re also pleased to add to the map two innovative power sector projects that are in planning stages. First, Systems International plans to begin construction in 2020 on twin facilities in Texas that can each produce 120 MW of carbon free electricity using a variety of fuel sources (everything from car tires to agricultural waste). According to the company, these facilities will have no smokestacks or water emissions, and they will capture all of their CO2 emissions (1.5 million tpy). The second project is a 1 GW electricity-generating facility that will power the “world’s first net-zero LNG (liquid natural gas) export and industrial gas production complex.”3 This facility also shows the CCUS synergies between the power generation and industrial sectors.

Bioenergy with Carbon Capture and Storage (BECCS)

BECCS projects capture the CO2 emissions from facilities that use plant materials to generate power or create fuels. Since the plants have absorbed carbon from the atmosphere through photosynthesis, BECCS can actually be carbon-negative in certain situations, if all of the facility’s emissions are captured and permanently sequestered. That makes this application especially important for meeting emissions reduction goals. Unfortunately, the global BECCS project count has not grown beyond the seven projects identified in Third Way’s previous map. Overall, the sector is underperforming despite studies emphasizing that BECCS costs are among the cheapest of any application. This is especially true for CCUS projects on U.S. ethanol facilities.4

Industrial Facilities

Industrial emissions are responsible for up to 29% of the United States’ total carbon footprint,5 and industry is the only sector expected to see a significant increase in emissions over the coming decades.6 The deployment of CCUS will be critical for addressing this hard-to-decarbonize sector of the economy.7 The good news is that in the last two years, ten new industrial carbon capture projects have been initiated around the world, bringing the total up to 76. Two of the most innovative, new large-scale industrial CCUS projects are in the U.S.8

In May of 2019, Wabash Valley Resources announced what could be the largest carbon sequestration project in the country, capturing up to 1.75 million tpy from a chemical facility in Indiana. This innovative project will not only cut the direct emissions from the ammonia it produces but will also indirectly reduce the carbon intensity of ethanol produced from the feedstocks that the low-carbon ammonia fertilizes. That ethanol then becomes more valuable in the California Low Carbon Fuel Standard market, demonstrating how industrial CCUS could spur an entire new carbon economy. In addition, Svante Inc., Lafargeholcim, Oxy Low Carbon Ventures, and Total recently launched a study to design a capture facility at the Holcim Portland Cement Plant in Florence, Colorado. This will be one of the world’s largest industrial capture facilities at 725,000 tpy, and among only a handful of projects in the cement industry, which generates an astonishing 8% of global emissions.9

A few other industrial CCUS projects across the globe have us excited. Santos, an Australian oil and gas producer, announced a FEED study for a 1.7 million tpy capture project on natural gas processing facilities in South Australia. The company reports that this project could eventually scale to 20 million tpy. In addition, Dalmia Cement, a large Indian company with 16 production facilities, is launching a capture plant at one of its factories in Tamil Nadu. This facility aims to capture 500,000 tpy, close to the scale of the Holcim cement plant in Colorado. Finally, the city of Leeds in the U.K. is planning a 1.5 million tpy capture project on hydrogen production facilities that use steam methane reforming, and will bury their captured CO2 underneath the North Sea.

Direct Air Capture

With the potential to remove significant amounts of CO2 directly from the atmosphere, direct air capture (DAC) is a unique and critical tool to help keep the global temperature increase to 1.5°C. But analysts estimate that DAC facilities will need to achieve a capture and permanent sequestration rate between 560 and 1,850 million tpy in order to reach net zero emissions by 2045.10 Our map shows that DAC still has a very long way to go to have this level of climate impact. There are currently eight DAC projects across the globe, and only one of them is a new addition since 2018. The good news, however, is that this new project will dwarf all other DAC facilities. Last year, Oxy Low Carbon Ventures announced that they will commence construction in 2021 on the world’s largest DAC facility in West Texas using Carbon Engineering’s technology. This giant project will capture between 500,000 and 1 million tpy – orders of magnitude greater than the next largest project (the 1,000 tpy Climeworks facility in Switzerland). We can’t underscore enough how significant this progress is but hope that policies allow for a more rapid global expansion of DAC projects in the coming decade.

Carbon Use

Carbon use projects transform carbon emissions into valuable products. It is the only major application on our map that focuses on the post-capture application of CO2. While most CCUS project databases do not closely track these projects, they represent one of the most important and fastest growing segments of the carbon capture industry. We’re excited to report that in the past two years there has been a 42% increase in the number of carbon use projects (from 147 to 209). Moreover, 52 of the 62 new projects are in the U.S. Novel applications for captured CO2 speak to the growing market for carbon use products. It’s important to note that our map only includes carbon use projects that sequester or displace carbon emissions. Thus, we do not feature applications like carbonated beverages.

The greatest current use for CO2 (by total number of projects, not volume of CO2 used) is in concrete manufacturing. In this process, CO2 is converted into a nano-sized calcium carbonate mineral that gets added to concrete mixtures and increases the overall compressive strength of the product. Since 2018, we count 44 new concrete mixing facilities in the U.S. that incorporate captured CO2, which brings the total number to over 100 projects (an increase of 71%).

Aside from concrete, a diverse array of carbon use companies has popped up all over the U.S. in the last two years. E3 Tec based in Illinois is working to convert CO2 captured from industrial exhaust sources to high-value industrial chemicals. HY-TEk Bio in Maryland is using CO2 captured from industrial flue gases to grow algae which can then be sold to make things like pharmaceuticals, cosmetics, paint, and bioplastics. Algae to Energy LLC., is producing a carbon-negative biofuel from algae. Companies in California and Colorado are converting agricultural biomass into biochar that can sequester carbon in soils. Even the fashion industry is getting in on innovative new uses for carbon dioxide. ADA Diamonds in California is producing synthetic diamonds out of captured CO2, and 10X Beta in New York City is partnering with Novomer to turn CO2 into plastics which can then be turned into carbon negative shoes.

Test Centers

Test centers are the final application on our map. These research facilities either self-identify as test centers specializing in carbon capture research, or they are part of the International Test Center Network (ITCN).11 The latter group of facilities was co-founded in 2012 by the DOE’s National Carbon Capture Center in Alabama and Technology Centre Mongstad in Norway. It aims to accelerate CCUS deployment across the globe. These centers share technical insights with each other and seek to reduce construction and operation costs for large-scale power generation and industrial capture projects.

Since 2018, we’ve added eight new test centers to the map bringing the total to 17. Several countries have become part of the ITCN. Japan, Germany, and Canada joined the Coalition, and South Korea’s Institute of Energy Research added two of its facilities. Australia also expanded the ITCN family with a pair of its research facilities, and the University of North Dakota’s Energy & Environment Research Center joined as well. These new test centers will help maximize the impact of coordinated CCUS R&D resources and reduce barriers to deployment.

Where Do We Go from Here?

An expanding CCUS universe means new economic opportunities around the globe and across the U.S. Our map shows that projects are underway or operating in 37 states and the District of Columbia. But with diverse applications ranging from DAC to diamonds, there is potential for rural, suburban, and urban communities in every state to participate in CCUS industries.

An expanding CCUS universe is also good for climate, especially if it enables the growth of certain applications that are particularly important for slashing economy-wide emissions. Yet analysts estimate that more than 2,000 large-scale CCUS facilities will be needed globally by 2040 to meet emissions targets, a far cry from the handful of dots currently on our map.12

CCUS projects have certainly been on the rise, but this industry has a long way to go in order to reach its full economic potential and contribute to climate efforts at the level scientists say is needed. Sound policies will accelerate the growth of CCUS projects across the U.S. Based on trends we’ve observed in our map, here are three basic policy principles that can help fill the map with new dots.

- More large-scale projects needed quickly. There are nineteen large-scale, operational CCUS facilities in power generation and industry across the globe.13 In order to realize a drastic increase in big projects, governments will need to invest in demonstrations that pave the way for additional projects and create more incentives that encourage broader deployment.

- Focus on RD&D in underrepresented CCUS applications. There are no operational CCUS projects on natural gas power plants in the U.S., no operational DAC facilities, and no operational projects in some of the highest-emitting manufacturing sectors. A concerted effort in innovation (with increased resources) should be directed at these sorely needed CCUS applications.

- Build the infrastructure and more projects will come. The map shows significant underground CO2storage potential in the U.S. and a growing number of carbon use projects. Yet, many investors will not consider developing a capture project unless they can affordably transport the CO2 to a storage or use site, and more carbon storage and use sites will not be developed until CO2 is readily available. As it did with the U.S. interstate system, the federal government should invest in a robust interstate carbon transport network that allows CCUS projects across the country to connect to storage sites and CO2