Report Published September 20, 2016 · Updated September 20, 2016 · 29 minute read

To Grow New Businesses, Improve Access to Credit

Takeaways

- New businesses play an outsize role in job creation in the U.S. economy, so the recent slowdown in new business growth should be of particular concern to policymakers.

- Research shows that there are gaps in borrowing opportunities for new and small firms, which may explain part of the slowdown in new business growth.

- Bank lending to large businesses has surged to new highs during the recovery, but lending to small businesses has failed to return to pre-recession levels.

- We explore four theories on what’s restricting the flow of credit: the creditworthiness of borrowers, the consolidation of the banking industry, new regulatory barriers, and market imperfections.

Uber, Warby Parker, Dropbox. What do these businesses have in common? Ten years ago, none of them existed. Today they are at the forefront of revolutionizing their respective industries. The online file-hosting service Dropbox, for example, is only nine years old. Yet it has nearly 500 million customers, provides 1,500 knowledge-based jobs, and supports thousands more.1

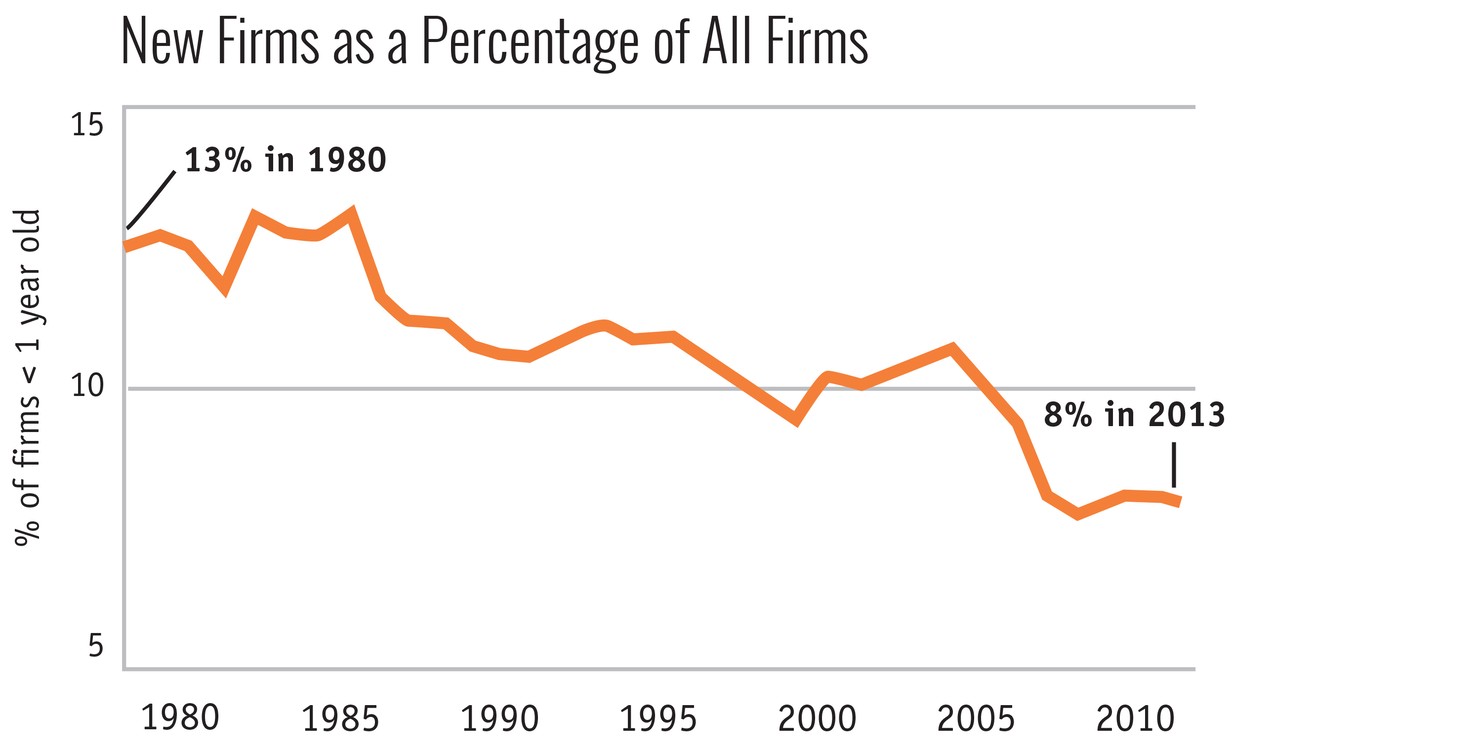

It’s no wonder, then, that new businesses such as these have a tremendous impact on the economy, domestically and abroad: New business startups, or firms in their first year, account for about 20% of U.S. gross job creation.2 Yet in the current U.S. economy, new businesses comprise only 8% of all firms, compared to 13% in 1980. This relatively disappointing startup rate is an important piece of the plodding expansion of the U.S. economy and the middling jobs market. While the headline unemployment rate is low, we still need millions more jobs to bring labor force participation rates back to pre-crisis levels for prime-age workers. As the slack in the labor market disappears, wage hikes will inevitably accelerate. But first, we need to figure out what’s holding back the creation of new businesses—and what’s slowing down their expansion after they launch.

This paper examines one of the factors holding back new businesses, access to credit, and explores four theories on what’s holding back lending to these critically important firms.

New businesses are critical to U.S. job growth

New businesses come in two varieties, traditional and transformational.3 Traditional firms represent the vast majority of new businesses: Think businesses like the new restaurant that opened down the street. Traditional firms usually follow an established business model providing services and goods to the local community. Traditional businesses play a critical role in our labor market, because they provide job seekers the opportunity to create their own jobs for themselves and others in their community. In particular, workers whose educational or employment histories do not meet the requirements of larger, more established firms can find their niche in the economy by starting their own traditional businesses.

Transformational firms play a distinct and particularly important role in the economy. They exist to innovate and subsequently disrupt an industry. The majority fail, but the remainder generally experience high growth. Here, you can think of Solar City, the company delivering clean energy to millions of households by designing, financing, and installing solar panels. Solar City, founded in 2006, now employs 13,000 workers. Surviving transformational firms expand jobs at a faster rate than other new businesses, and more than older firms.4

Here’s another way to look at the jobs impact of new firms. Businesses that are less than a year old have added, on average, 2.9 million jobs annually between 1980 and 2010. Even 10-year-old businesses add jobs at a faster clip than businesses aged 16 years and older. Finally, high-growth firms—those that increase their employment by at least 25% annually—are disproportionately young.5

Source: Third Way, Ready for the New Economy, 20156

While new businesses continue to play an outsize role in the U.S. economy, there just aren’t as many of them as there used to be. The start-up rate of new businesses has steadily declined over the last few decades. In 1980, firms in their first year accounted for 13% of all companies. But since 2010, that rate has hovered near 8%. Just as concerning is the fact that, while new businesses still punch above their weight in job growth, they are not creating jobs at the rate they used to. In 2011, the average new business hired 4.4 workers, whereas in the 1990s it hired 7.3.7

The rest of this report will address the challenge of credit access that new businesses face. But first, a quick note on terminology. While some of our findings are drawn from studies focusing exclusively on new businesses, others are from studies on small businesses—some of which are younger in age, but many of which are not. For example, in the 2015 Small Business Credit Survey led by the New York Fed, 55% of the small businesses studied were between 0-10 years old, and 21% were two years old or younger.8 We choose to include that research, because there is substantial overlap of these two types of firms, and because the challenges facing them are similar.

Access to credit is a problem for new businesses

Numerous factors can determine whether a startup fizzles out, plateaus, or scales to a booming business. Yet nearly all businesses need credit to expand when they are young. Because they are small and privately held, they cannot access public capital markets—and likely have no hope of doing so for years. So their only options for equity are typically the savings of the owner(s), relatives, and angel investors, and eventually for some firms, venture capital. That leaves lending—in a variety of forms—as the most accessible form of financing for most new businesses. Even new businesses that have succeeded in attracting outside investors rely more heavily on lending than larger, established firms.9

When the regional Federal Reserve banks surveyed new and small business owners in 2015, startup owners ranked credit availability as their fourth most important business challenge, behind cash flow, costs of running a business, and hiring qualified staff. Furthermore, microbusinesses (firms with annual revenue under $100,000) and startups (firms under two years old) have a harder time accessing credit than their peers. In fact, 63% of microbusinesses and 58% of startups were unable to fulfill their funding needs.10 This is not new. Going back to 2006, well before the recession, the National Federation of Independent Business’ monthly survey already began to show that small businesses were experiencing rougher credit conditions than in previous years.11

While it would be too simplistic to hold credit issues out as the sole binding constraint for new business growth, it is fair to say access to credit is among the top handful of challenges that can make or break a new business. In particular, there are three categories of lending in which small businesses experience vastly different outcomes, depending on the type of lender.

Personal credit

For the youngest and smallest startups, the first place to turn for credit is the consumer lending space. Because their firms have little or no credit history or revenue, bank loans can be extremely difficult to obtain. Thus, these business owners turn to personal sources of funding—credit cards and home equity, in particular.

Unsurprisingly, it’s more common for firms with fewer employees to use personal credit cards for business purposes. The percentage of small business owners using a personal credit card rather than a business credit card grew during the recession, from 42% in 2009 to 45% in 2010 to 49%, or just under half, in 2011.12

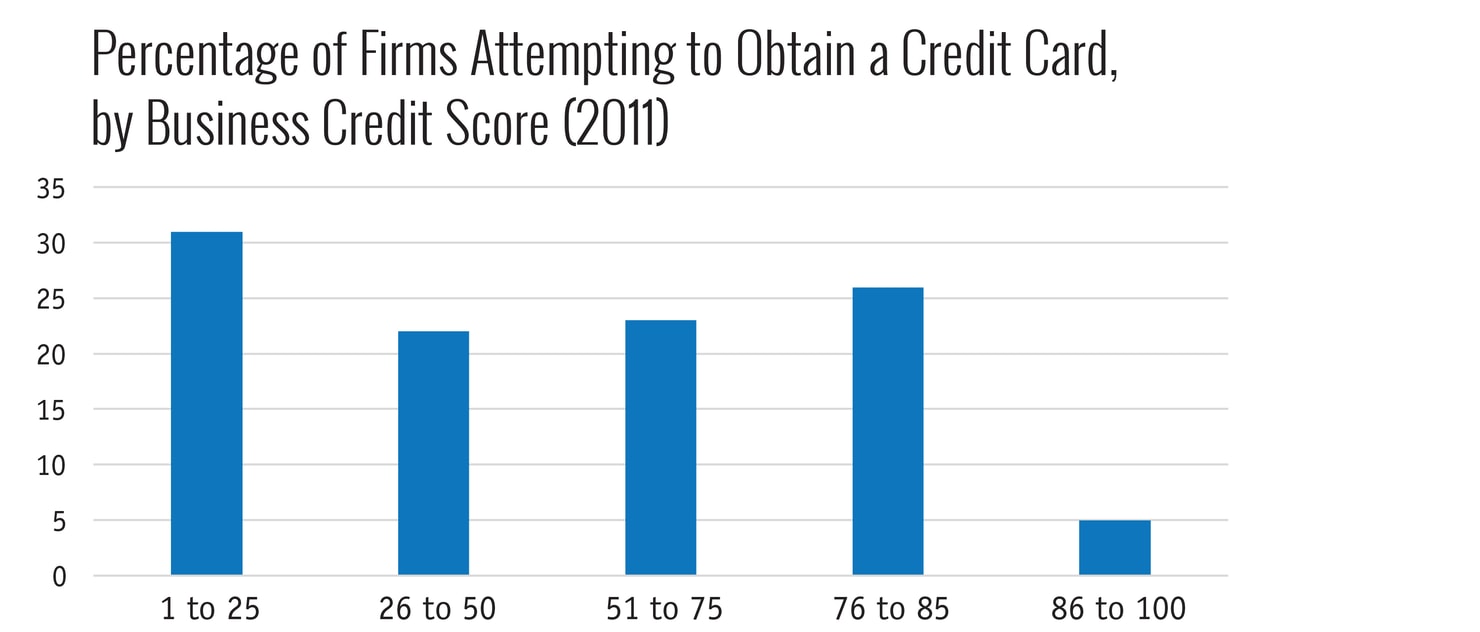

Firms with lower business credit scores tend to have higher demand for credit cards, as seen in the chart below. Newer and smaller businesses are more likely to have lower scores because they are in the process of building a credit record. Despite this, credit cards are usually easier for smaller businesses to obtain than other forms of credit. For example, last year microbusinesses reported a 76% approval rate for credit cards, compared to a 65% approval rate for business loans and credit lines.13

Note: Business credit scores are distributed on a scale of 1 to 100. Source: National Federation of Independent Business, “Small Business, Credit Access, and a Lingering Recession,” 2012, Table 5.14

But credit cards tend to have a limited purpose. For the most part, small business owners use credit cards because they are a convenient way of making payments, rather than their ability to carry a balance forward.15 Those that do have large credit card balances often find themselves unable to access additional credit. Therefore, loans are still critical for firms looking to grow and invest.

In the wake of the recession, it’s no surprise that access to personal credit dried up. The amount of revolving consumer credit outstanding fell by nearly one-fifth from its high of $1 trillion in April 2008 to its April 2011 low. It has taken five years to recover.16 But this is a fraction of the size of the mortgage debt market, which peaked at $14.8 trillion in 2008, fell to $13.2 trillion in 2013, and now stands at $13.8 trillion.17 And a fair amount of small business owners use their homes to fund their businesses. A 2011 National Federation of Independent Businesses (NFIB) survey of small business owners found that 14% have put proceeds from their home mortgage toward their business, and another 11% use their home as collateral for a business loan.18

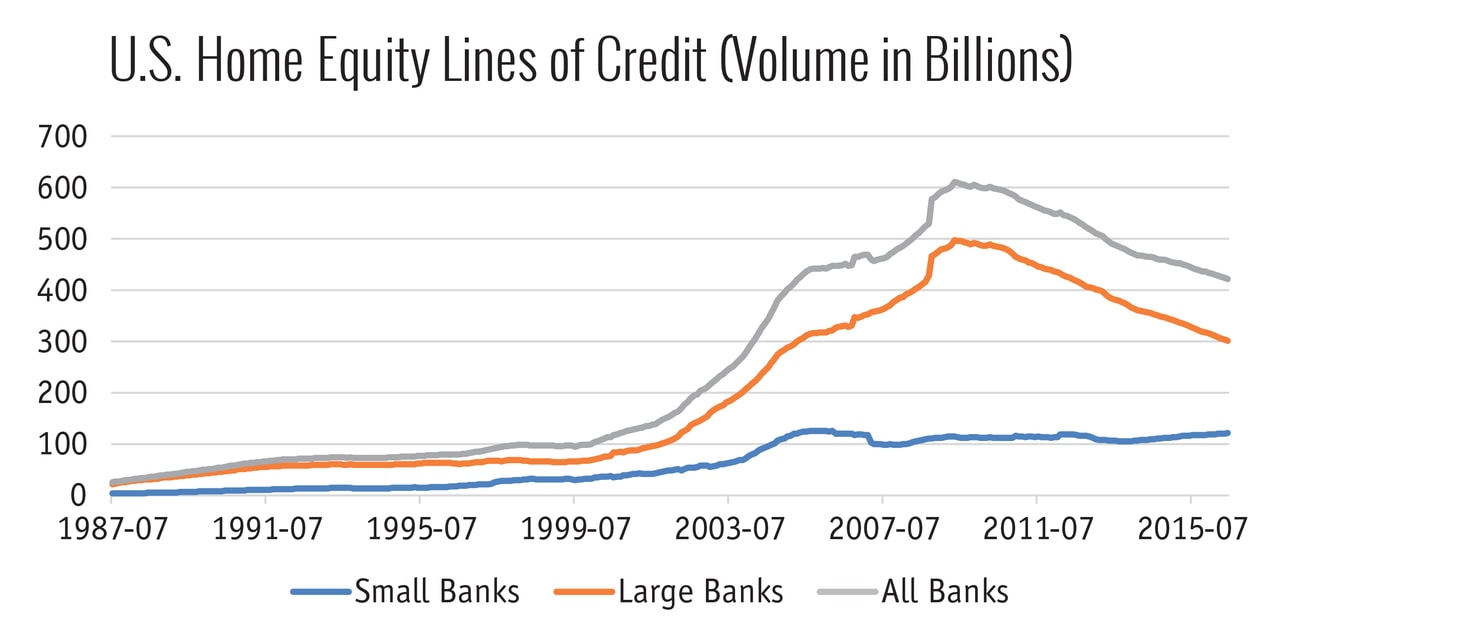

Business owners’ largest asset to post as collateral is often their home, so the plunge in home values had a direct effect on how much they could borrow. One way to evaluate this is to look at trends in home equity lines of credit, a form of revolving consumer credit. Home equity lines of credit peaked at $611 billion in April 2009. As of July 2016, they are down to $421 billion—a decrease of about 31%.19 This is almost entirely due to a pullback of home equity lines of credit offered by large banks. But small banks, which small businesses tend to prefer, have maintained their level of revolving home equity loans throughout the recession, recovery, and expansion.

Source: Board of Governors of the Federal Reserve System, Assets and Liabilities of Commercial Banks in the United States. Retrieved from the Federal Reserve Bank of St. Louis Economic Research (FRED).

Commercial bank loans

Obtaining a commercial bank loan is an important milestone for new and small businesses, because these loans typically come with lower interest rates than those of credit cards and allow the owner to put less of his or her personal assets at risk. While success obtaining a commercial bank loan is never guaranteed, especially for new and small businesses that may not have a robust credit history, it appears that it has gotten tougher in recent years.

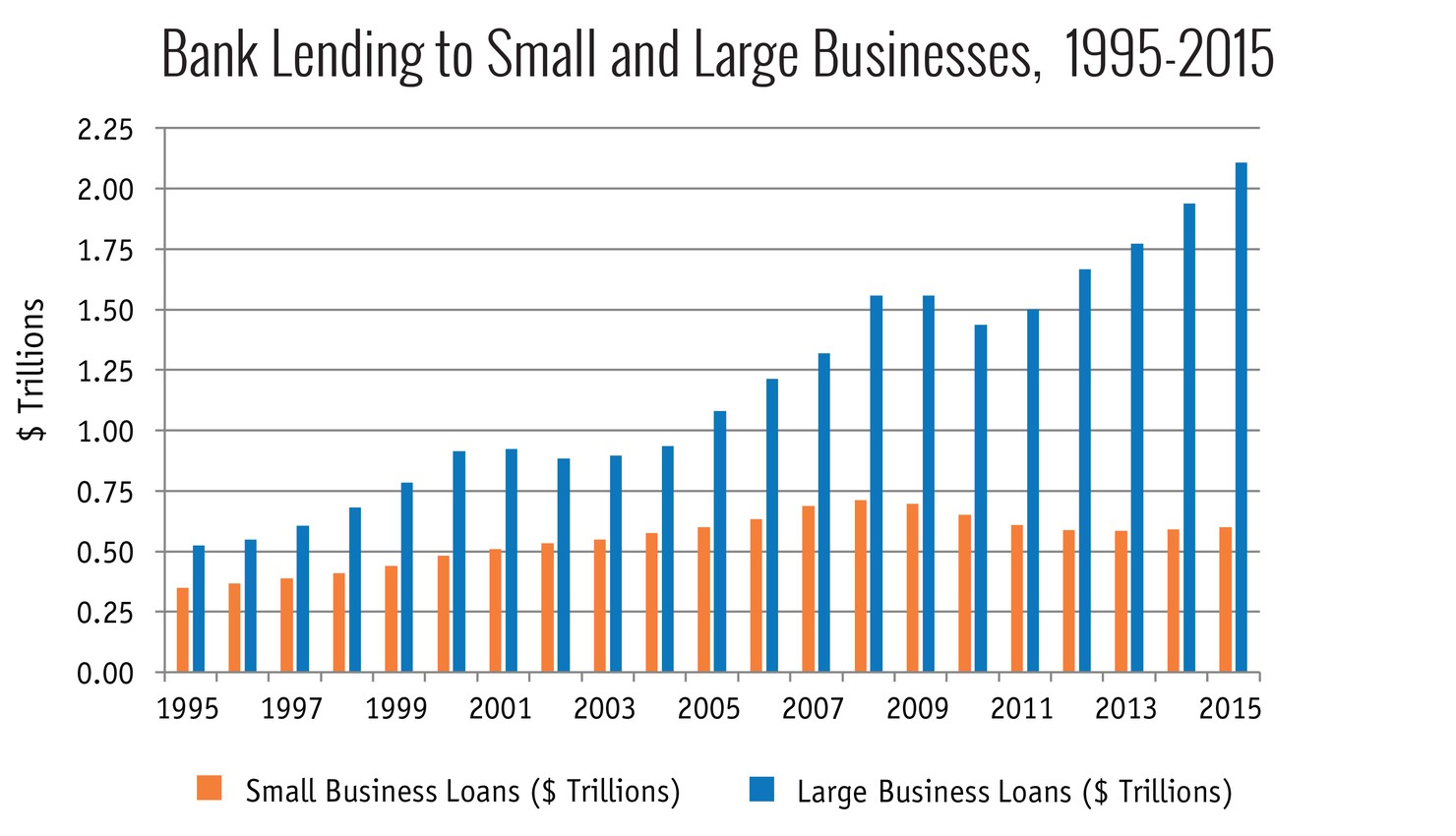

While big businesses have enjoyed a 35% increase in bank lending since 2008, small businesses have faced a 15% decrease.

One of the most comprehensive studies in recent years to assess this issue was a 2014 Harvard Business School paper by Karen Mills, the head of the Small Business Administration (SBA) from 2009 to 2013, and Brayden McCarthy. The report concluded that bank credit for small business was in steady decline since well before the 2008-2009 financial crisis and the new regulations that followed. Specifically, the study concludes, the credit environment for small businesses has been more depressed than the economic environment has warranted. During the recovery, banks have been more risk averse in general.20

What’s also concerning, though, is that new and small businesses are experiencing a very different lending environment from larger, more established businesses. For big businesses, bank lending has skyrocketed since the recession ended, to a new high of over $2 trillion in 2015. But for small businesses, bank lending has plateaued. While big businesses have enjoyed a 35% increase in bank lending since 2008, small businesses have faced a 15% decrease.21

Part of the problem is that bank business models are changing in an attempt to reduce risk, from both a regulatory and an operational standpoint. In response, many banks have taken the step of eliminating loans to businesses with revenue below $2 million, for example, or to stop making loans less than $100,000 altogether. Instead, banks sometimes refer these small business owners to credit cards with much higher yields than commercial loans. Other banks aren’t making any commercial loans less than $250,000.22

The chart below, compiled by Professor Rebel Cole of DePaul University, demonstrates how large this gap has become. In this chart, small business loans are defined according to the commonly used threshold of $1 million or less for commercial and industrial loans and commercial real estate loans. There has been a significant decline in the volume of these loans since the recession, and it still has not bounced back.

Note: The size of Commercial and Industrial loans and Commercial Real Estate loans are used by many researchers as a proxy for distinguishing small business loans from large business loans. Small business loans are considered to be C&I and CRE loans under $1 million. Source: Federal Deposit Insurance Corporation (FDIC) call report data compiled by Rebel Cole.

Online lending

One recent development for new business borrowers is the rapid rise of a new source of credit: nontraditional, online lenders. According to a recent report by the Treasury Department, online marketplace lending has grown from $1.2 billion in small business loans in 2014 to $1.9 billion in 2015, an increase of almost 60% in just one year.23 This is about 3% of the marketplace for small business bank loans.

Whereas traditional banks rely on small business owners’ personal credit history in making lending decisions, online lenders use algorithms drawing upon a variety of data, including credit histories, revenue patterns of the business, and—in some cases—social media sources like Yelp reviews.24 This allows online lenders to approve or deny applications much more quickly than traditional banks. While financial technology advocates have cheered the development of these platforms, some critics have voiced concerns about privacy and appropriate use of social data. And others have questioned whether they are capitalized enough and are regulated as prudently as traditional banks.25

Two of the most prominent online lenders are OnDeck and Kabbage. These firms are known as online balance sheet lenders, because they themselves are making the loans. These lenders have focused on shorter-term loans, averaging about nine months, which businesses typically use to manage cash flow. Interest rates tend to be high, with Annual Percentage Rates (APRs) ranging from 30% to 120%. That’s anywhere from two to eight times as much as the APR on credit cards, which currently average 15%.26 And it’s three to twelve times as much as getting a personal loan, which currently costs 9-10% in annual interest for a two-year loan.27

Other new lenders, like Lending Club and Prosper, facilitate loans from investors to new businesses. These loans typically range from three to five years, and funds are often used to repay credit card debt or other high interest loans. Their interest rates range from 8% to 24% for a three-year, $250,000 loan.

According to a 2015 survey, 20% of small business owners had applied for a loan from an online lender, and 71% were approved for at least some credit. However, the usefulness of online lenders to small business has been limited. Small businesses give online lenders lower satisfaction ratings than traditional banks because of their unfavorable repayment terms and relatively high interest rates.28 Although online lenders may have a promising role in the future of small business lending, they have not yet matured enough to resolve the credit access problem that new and small businesses face.

Four theories on the new business credit problem

1) Creditworthiness

There’s risk inherent in extending a loan, but it can be reduced by confirming the borrower’s creditworthiness. A common framework used to evaluate creditworthiness is known as the “Five C’s”: Character, Capital, Capacity, Conditions, and Collateral. The Five C’s help lenders evaluate a borrower’s ability to repay. A firm meeting the quantitative thresholds associated with each of these five indicators is likely to qualify for a loan. This is described as fitting into the “credit box.”

The Five C’s can be understood as an assessment to determine whether a firm can make repayments on time and where the repayment will come from. In normal economic times, repayment would generally come from cash flow, but when times get tough, lenders want to ensure that a firm has the resources to make up a shortfall. Lenders also want to see that business owners have “skin in the game,” meaning that they are able to take on losses to meet their promise to repay the loan.

A Comparison of the Creditworthiness of Established Versus New Businesses

| Indicator | Measurement | Established Business | New Business |

| Character | Business credit score | Business credit score readily available; score reflects previous repayment history | Personal credit scores typically used; business credit score reflects perceived repayment ability |

| Capital | Owner's investment | Multiple shareholders with higher ability to bear losses | Small number of partners or single owner with limited ability to bear losses |

| Capacity | Cash flow | History of income statements with profit and loss records | Credit inquiry may predate launch of business and/or sales |

| Conditions | Interest rate spreads | Adverse macroeconomic and market conditions may outweigh the firm's credit record | Adverse macroeconomic and market conditions may outweigh the owner's personal credit record |

| Collateral | Assets | Property, equipment, and other assets have been built up by the firm over time | Property, equipment, and other assets belong to owners personally |

Firms that fit into the credit box should have little trouble getting approved for a loan. New firms and small businesses, however, have difficulty meeting the standards of the Five C’s framework because they are unlikely to have much of a tangible track record to prove their ability to repay a loan. In fact, according to the 2015 Small Business Credit Survey, the top reason why growing, startup, and micro businesses were denied credit is insufficient credit history. The second most common reason for two of these categories, growing and micro businesses, is insufficient collateral.29 Generally, many new and small businesses just have not been in operation long enough to establish consistent cash flow or accumulate assets.

Only 50% of new and small business applicants surveyed by the regional Fed banks received the full amount of credit financing they sought last year.

A new business can still receive a credit score if it does not have a credit history, but there’s a catch. To construct a score, credit rating agencies may refer to records from comparable firms. The most common characteristics agencies use to develop a projection are firm age, size, and financial situation. From there, they look at that peer set’s repayment record to extrapolate what it might be for the firm under consideration. Here’s the problem: Younger firms are more likely to be unprofitable.30 Therefore, a comparative analysis may put a new business seeking credit at a disadvantage, since its peers are less likely to be successful than older firms, where more unprofitable firms have been winnowed out.

Due to the creditworthiness conundrum, only 50% of the full panel of new and small business applicants surveyed by the regional Fed banks received the full amount of credit financing they sought last year. Of the other 50%, 14% received at least half of their request, 18% received less than half, and 18% were denied outright.31 This leads many new and small business owners to either use personal funds to supplement or replace what they hoped to receive in a business loan, or delay plans to expand, invest in new resources, or hire additional employees.

New and small business owners are well aware that their attributes make them less likely to be successful in getting a business loan. Unfortunately, this leads many of them to not even try. Last year, nearly half of the businesses under two years old that participated in the Small Business Credit Survey did not apply for financing because they assumed that they would not qualify.32

Last year, nearly half of the businesses under two years old that participated in the Small Business Credit Survey did not apply for financing because they assumed that they would not qualify.

This reluctance to apply for credit may be a symptom of a much larger issue—that is, that small business demand for credit has fallen in general. As Fed Chair Janet Yellen put it at a June 2016 Congressional hearing, “We meet with many banking organizations to discuss this issue, and they say the demand for credit by small businesses and medium-sized businesses remains somewhat depressed. But I think the supply and availability of credit are there.”33 The question is what might be causing the reduced demand. Is it simply that new and small business owners do not need or want to apply for credit? Or is it that new and small business growth is lower than expected?

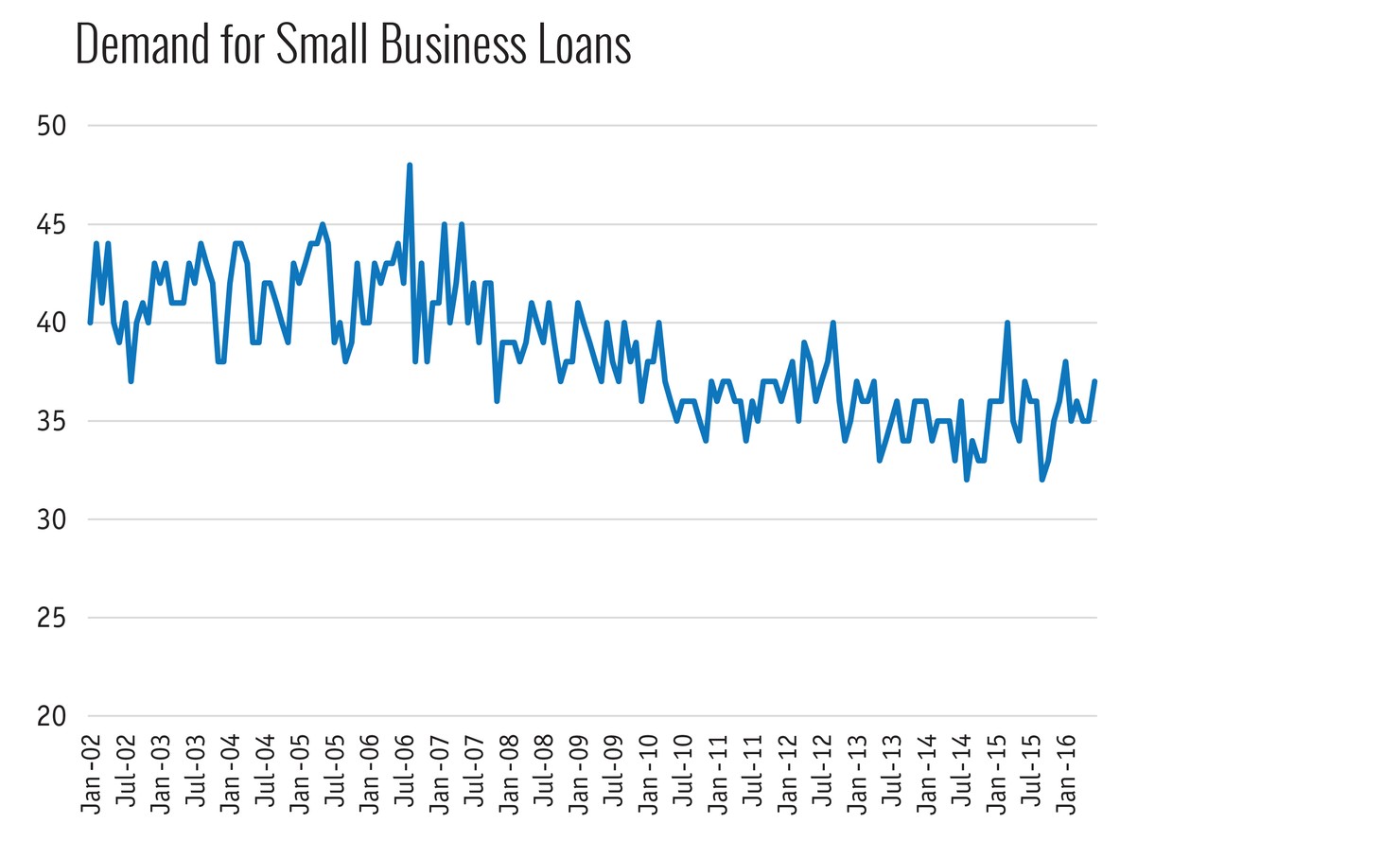

The answer is likely due to both. In the chart below, we have constructed an index of demand for credit based on the percent of respondents who indicated that their borrowing needs were or were not satisfied in the NFIB’s monthly Small Business Economic Trends survey.34 Overall, the percent of respondents seeking to borrow at all has fallen from an average of 41% in 2002 to an average of 36% in 2015.

Source: National Federation of Independent Business, Small Business Economic Trends

But it should also be acknowledged that many small businesses were unable to survive in the financial crisis and its aftermath, and that could well be the reason for lower demand. Census data shows that 365,000 businesses with fewer than 500 employees disappeared between 2007 and 2011. That means lost business growth, too. A report by Goldman Sachs estimated that there would have been 600,000 more small businesses in 2012 had the recovery from the most recent recession followed historical trends.35 And it may not just be the recession that is at fault. A new report by the Roosevelt Institute suggests that the decline in entrepreneurship is the result, rather than the cause, of reduced demand for labor dating back to 2000.36

2) Banking Consolidation

The share of total assets held by banks under the $1 billion threshold has dwindled during the era of bank consolidation to 8.1% by last year.

While the U.S. banking industry remains highly fragmented compared to its international peers, it is widely recognized that it has gone through a long period of consolidation. The number of banking institutions has decreased by two-thirds over the last 30 years.37 More than half of this decline is due to mergers. (The FDIC notes that two-thirds of bank mergers involve a small bank acquiring another small bank.)38 About one-third of the decline can be attributed to interstate banking deregulation, and the remainder is the result of bank failures.39

Of the 5,260 banks remaining today, more than 90% operate as community banks.40 Community banks generally have less than $1 billion in assets, engage in traditional lending activities, and serve a limited geographic area.41 However, the share of total assets held by banks under the $1 billion threshold has dwindled during the era of bank consolidation to 8.1% by last year.42

A report commissioned by the SBA in 2012 found that smaller banks expand both small business lending and business lending overall at higher annual rates than larger banks.43 But surveys conducted by the NFIB between 2009 and 2011 found that fewer small business owners are using regional and local banks for their business. Both regional bank and local bank use dropped by four percentage points each over that three-year span.44 Some policymakers have expressed concern that the overall consolidation trend will continue to reduce the number and influence of community banks, which will in turn reduce the level of small and new business lending.

The business model of community banks, which emphasizes relationship-based financial services, is considered to be more conducive to new and small business loans than that of larger banks.45 Credit unions, which are similar in size to community banks, are also frequently sought out by new and small businesses. Smaller banks are typically closer to the community and thus more willing to extend credit based on “soft” information, such as the lender’s personal knowledge of the borrower, his or her business, and the community that the business serves.46 Indeed, the 2015 Small Business Credit Survey notes that loan applicants were successful 76% of the time at small banks, versus 58% of the time at large banks.47

On the other hand, larger banks are often able to offer loan products at less expensive rates because they can achieve greater economies of scale. For example, according to the Fed’s Survey of Terms of Business Lending for the second quarter of 2016, large domestic banks charged an average interest rate of 3.55% on loans between $10,000 and $99,999, while small domestic banks charged 4.62%.48 The one percentage-point difference in this spread could be considered not only the cost of different economies of scale, but also the cost of making a riskier loan on soft information, as opposed to a relatively safer loan that fits neatly into the credit box.

So, which type of bank is more likely to make small business loans? It depends whether you look at it from a relative or absolute basis, as demonstrated in the charts below. On a relative basis, smaller banks dedicate larger shares of their lending portfolios to small business loans (21% versus 4%). Larger banks, however, lend more to small businesses on an absolute basis ($2.6 billion versus $925 million). Ultimately, the ongoing wave of bank consolidation may bring down the costs of small business loans, but it could also make it more difficult for new and small businesses to qualify for loans.

Snapshot of Weekly Business Lending Volume for Large and Small Banks

| Distribution of Business Lending | Amount of Business Lending | ||||

| Loan Size |

Large Banks |

Small Banks |

Loan Size |

Large Banks |

Small Banks |

| $10K-$99K | 4% | 21% | $10K-$99K | $2.6B | $925M |

| $100k-$999K | 16% | 52% | $100K-$999K | $9.3B | $2.4B |

| $1M-$9.9M | 27% | 27% | $1M-$9.9M | $15.8B | $1.2B |

| $10M and up | 53% | N/A | $10M and up | $31.1B | N/A |

| Total | 100% | 100% | Total | $58.8B | $4.5B |

Source: Board of Governors of the Federal Reserve, “Survey of Terms of Business Lending”

3) Regulation

President Obama signed the Dodd-Frank Wall Street Reform and Consumer Protection Act into law on July 21, 2010. Six years later, it continues to be the subject of debate about the intent and consequences of financial regulation. There is strong evidence that our economy is safer and better off after Dodd-Frank than before it. Yet, policymakers and advocacy groups have expressed concern that community and small banks bear a disproportionate regulatory burden from the legislation. A number of community banks have cited CFPB mortgage rules, stress testing, and financial disclosures as burdens on their businesses. In turn, this has a dampening effect on small business lending, because small banks are popular lenders to small businesses.

The best evidence of Dodd-Frank hampering small business lending relates to compliance costs. Banks of all sizes have reported an increase in compliance requirements since Dodd-Frank. This is particularly burdensome on community banks, which face greater obstacles dedicating the time and resources necessary to recruit and train staff for this purpose, as detailed by a recent GAO study.49 In the view of some economists, these regulations essentially function as a tax that reduces investment. A report by the American Action Forum estimates that Dodd-Frank regulations impose a compliance burden that could modestly reduce GDP growth on the order of 0.06% annually, or an average of $89.5 billion per year over the next decade.50

Recent initiatives to increase bank capital requirements are also relevant to new and small business lending. Loans go onto banks’ books as assets, and these new rules require banks to hold higher ratios of equity against their assets. Although small business loans are not risk-weighted like mortgages and other types of loans are, they are still factored into the simple leverage ratio of equity to assets that banks are expected to meet. The Bank for International Settlements estimates that each percentage point increase to capital requirements adds 13 basis points to lending spreads.51 As loans become more expensive, businesses become less likely to seek them.

Despite these drawbacks, capital requirements are one of the most effective tools to stabilize the financial system. In fact, the same study by the Bank for International Settlements found that the enhanced financial stability generated by raising capital requirements, up to a certain degree, actually adds to GDP levels.52 That’s a good thing for new and small businesses, because less economic and financial volatility gives them a better chance of survival.

4) Market Imperfections

In any market, several conditions must exist for it to work efficiently. One is that buyers and sellers need to be able to access information about each other affordably. Will the seller follow through and deliver the product with the quality it has advertised? Online reviews, business ratings, and certifications can help answer this for potential buyers. On the flip side, will the buyer actually pay for the product it is purchasing?

When banks lend to larger, more established businesses, these questions are easier to answer. Lenders can review publicly available financial statements of the business and look at the company’s cash flow. But with new and small businesses, as mentioned previously, owners have difficulty conveying detailed information. This means it can take longer for a bank to process a loan application while it gathers information. In a 2015 survey, small business owners reported that when applying to borrow money from both small and large banks, their top complaint was the “difficult application process,” followed immediately by the “long wait” for a decision. These concerns far outweighed complaints about interest rates and repayment terms.53 The consequence of this slow process: small businesses take longer to find a bank willing to lend to them, which slows down their growth.

So what’s different now compared to the past? Fifteen years ago, the market for $100,000 to $1 million loans was more frequently serviced by locally oriented bankers, who used relationships and knowledge of the local economy to make lending decisions.54 That resulted in lower application costs and shorter wait times. Over time, banks have come to rely on more standardized application processes. And since it costs as much to underwrite a $100,000 loan as it does a $1 million loan, the payoff for those $100,000 loans just isn’t as big. Some banks are trying to fill the void by marketing their small business credit cards—like “Ink,” by JPMorgan Chase. Others, such as Bank of America, are offering smaller lines of credit.55 But these products aren’t enough to meet demand, which is pushing many small businesses toward online lenders. In that same 2015 survey, online lenders scored high marks for their approval speed. The downside: far higher interest rates.

Finally, a missing piece to the small business lending market may be one facet that helps facilitate other types of lending: securitization. Take mortgages, for example. Oftentimes when mortgage lenders underwrite a loan, they will sell that mortgage to an investment bank. The bank will package it with mortgages from other lenders to form a security that is sold to investors. By pooling mortgages together, risk can be spread out among investors, according to their desired risk. Securitization reduces the risk associated with individual loans, resulting in lower interest rates and likely a greater supply of lending.

There is a much smaller market for the securitization of small business loans. Online lenders like OnDeck and Kabbage have securitized small business loans. But the securitization market for traditional small business loans is largely limited to loans guaranteed by the SBA.56 The chart below shows that SBA-backed loans make up a small portion of bank lending—about 1% for large banks and 2% for small banks.

| Type of bank | SBA-backed loans as a percent of the value of C&I loans |

Total value of C&I loans |

Total value of SBA- backed C&I loans |

| Large domestic bank | 0.9% | $58.7 billion | $528.5 million |

| Small domestic bank | 2.0% | $4.9 billion | $98.3 million |

Source: Board of Governors of the Federal Reserve, “Survey of Terms of Business Lending”57

Because the standards and terms of small business loans are highly idiosyncratic, and because there is limited data to characterize the risk of these loans, it remains difficult to pool these loans together. However, if the demand for small business loan securitization were to grow, it is not difficult to imagine banks finding new ways to make more loans to more businesses.

Conclusion

Getting more new businesses off the ground is one of the core economic challenges for the United States. There are multiple public policy objectives that can help that effort: incentivizing people to become entrepreneurs; helping new firms attract and retain talent; modernizing regulations; providing quality infrastructure; and fostering a vibrant, efficient market for credit to new businesses.

How adequate is the credit market for new businesses today? There are several things we know with a good degree of certainty. The macro data shows that overall lending volume has recovered from its recession lows. But not for small and new businesses, which express dissatisfaction with their access to credit. They prefer to borrow from traditional banks, with a modest preference for small banks. But they face obstacles by bank lending processes, long wait times, and the growing difficulty of getting small-dollar loans. The emergence of online lenders is a recent addition to the sources of credit, but their rates are too high, according to many borrowers, and these lenders cannot yet fill the need for lending on the scale demanded by new and small businesses.

What’s less clear is whether the volume of lending to small businesses is below what economic conditions actually warrant. There is strong evidence that there are simply fewer creditworthy small businesses putting forward loan applications than in the past. Unfortunately, the best data available send conflicting signals.

So, where do policymakers go from here? First, Congress should fully fund research by the SBA, FDIC, Census Bureau, and the Fed, especially studies that provide insights about changes in the credit markets over time. Second, Congress should realize there’s no silver bullet. In fact, the pursuit of one objective above others could have dangerous consequences. A rollback of capital requirements, for example, could reintroduce an element of financial instability that contributed to the crisis.

However, it is reasonable that Congress could improve the lending environment for new businesses by trying to move the needle with modest changes from multiple angles: Maintain the historical role of credit unions and community banks. Find ways to reduce paperwork for these institutions and others making small-dollar loans. Create a regulatory framework for online lending that lays a strong foundation for the sector’s sustainable growth. Provide more opportunities for banks to securitize small business loans. These are all objectives that, addressed through modest, ongoing policy efforts, will help ensure that access to credit is not standing in the way of our economy’s growth engine.

—Jordan Baum contributed to this report.